Ireland‘s businesses are particularly bullish about their future prospects, with Irish business expectations the second strongest on a global level, behind only Brazil, the latest S&P Global Business Outlook survey has found.

According to the findings, Irish private sector firms have a ‘stable, positive outlook’ about output growth over the next 12 months, however inflationary pressures are expected to rise, both in terms of costs and output prices.

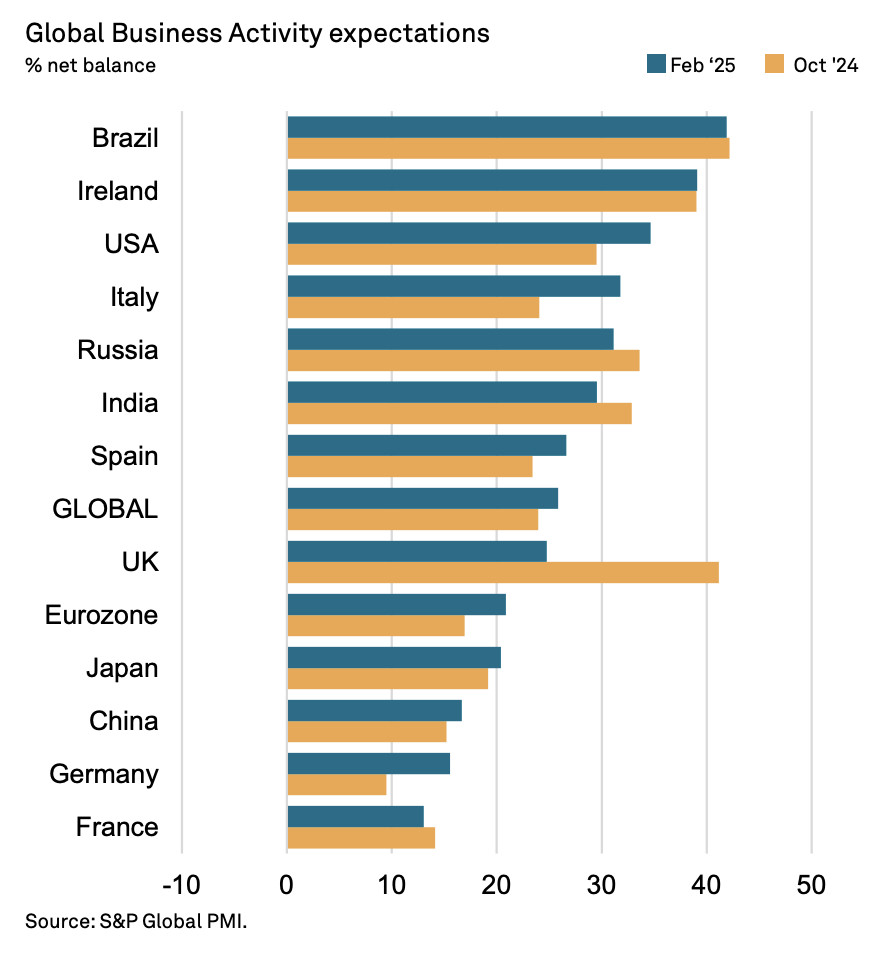

The data, which covers Irish business expectations up to February 2025, found that the headline net balance for business activity in the manufacturing and service sectors held steady at +39% for the month, in line with the figures reported last June and October.

This is slightly below the long-run average recorded since late 2009, but signals ‘robust optimism’, S&P Global said.

‘Comparatively upbeat’

“Irish companies remained comparatively upbeat on the business outlook at the start of February,” commented Trevor Balchin, economics director at S&P Global Market Intelligence. “Among the 12 nations for which manufacturing and services data are available, Ireland was the second most optimistic on output growth behind Brazil, and the joint-most confident on hiring.

“As always there is much uncertainty and risks to the downside, including unpredictable trade policies, a resurgence in inflation, rising wage costs and supply chains. On the other hand, companies are highlighting opportunities for growth linked to an economic recovery in Europe – the eurozone activity net balance rose to a two-year high.”

Workforce expectations

Irish businesses are also are confident about increasing their workforce, with the net balance for employment expectations standing at +22% – making the country the joint-most-confident when it comes to hiring plans, alongside Brazil and Russia.

Ireland also had the strongest outlook for profitability in Europe, at +25%.

Regarding capital spending, Irish firms largely expect growth, although the confidence level has slightly decreased from the previous quarter, and the outlook for research and development remains subdued, with a net balance of +2%.

“The latest figures on inflation expectations will be a concern,” Balchin added. “The staff costs net balance remained stubbornly high, while the non-staff costs and output prices net balances both jumped to the highest since late-2022. If inflation takes off again, that will make further interest rate cuts less likely, stymieing demand.” Read more here.